Market Behavior Ebb and Short Volume Flow

Last week we transitioned from shortening days and lengthening nights to lengthening days and shortening nights. It happened December 21st, when the Earth’s pole in the northern hemisphere reached its maximum tilt away from the sun.

Laws of physics determine planetary ebb and flow in the universe. And the wonder that unfolds is immune to our wishes. This whole spectacle in which we exist is unmoved by our desires.

Yet we have studied the fundamental mechanics of the universe deeply enough to understand some of its order. It was not a surprise when the winter solstice reversed the durations of days and nights on December 21st.

We do not need stories when we know the laws of physics.

Market behavior, like the universe, can be explained by stories or laws. In the case of the market, stories attract the most attention. They are born from clickbait, fueled by crowds, and validated by the great bias of hindsight. Our tendency to look back at events that were not predictable at the time and believe the outcome was easily predictable.

Market behaviors are governed by laws far less grand than universal physics. Yet they share an important trait: mathematical determinism. Meaningful explanations in the form of probabilistic analyses.

Observable for those who wish to study them.

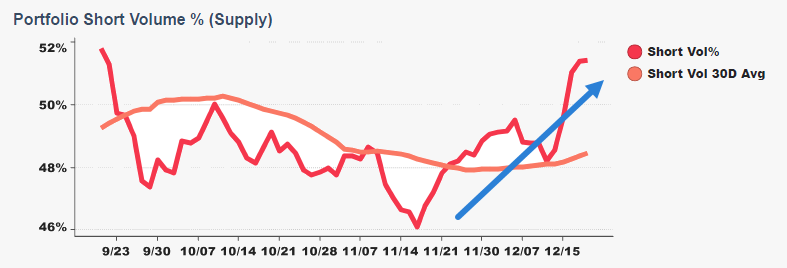

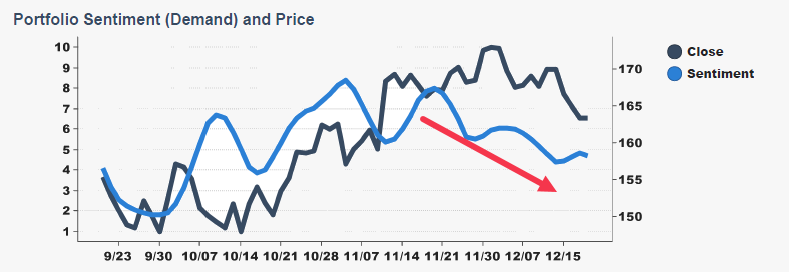

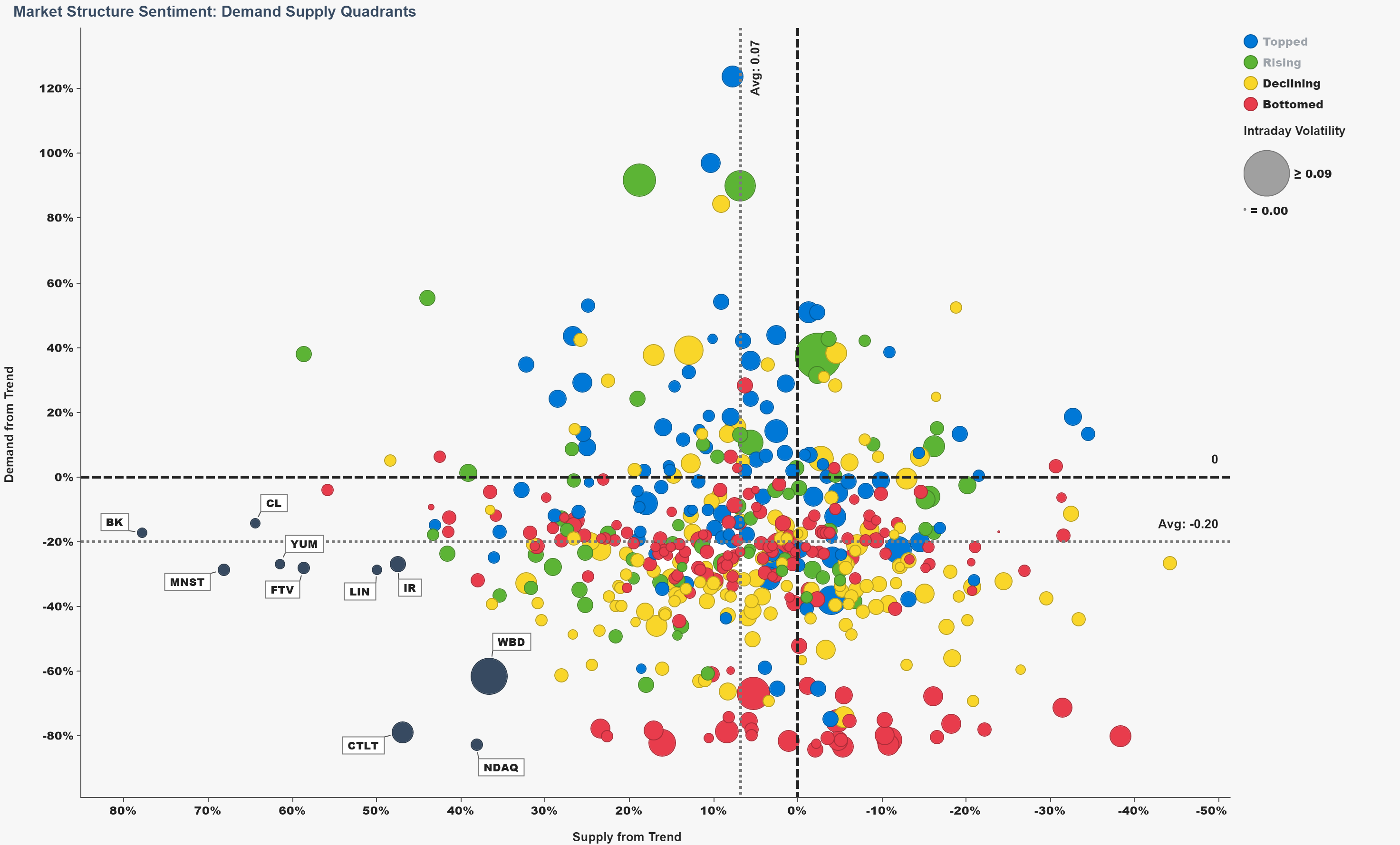

Let’s turn our attention to the morning of December 21st as daily light began to outlast darkness. Across the over the prior month, short volume rose from 46% to 52%, a significant 13% increase across this broad market proxy. Meanwhile demand fell from 8 to under 5 on its 10-point scale.

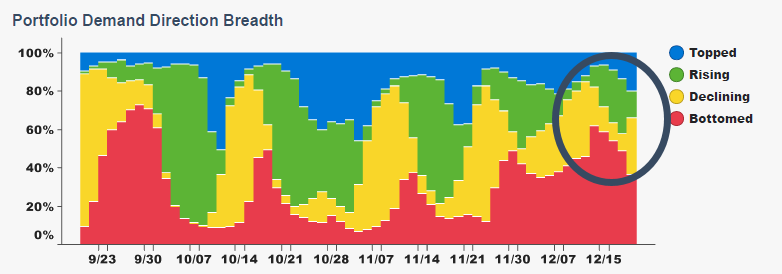

Further, since 12/16, the percent of stocks with rising demand halved from 28% to 14%. While the percent of stocks with falling demand more than tripled from 9% to 29%. All the while, fast money behavioral flow grew from about a quarter to a half of all market liquidity. Algorithms amidst expirations.

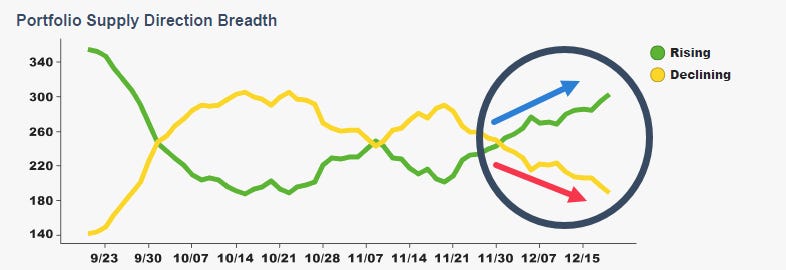

And our supply breadth ratio reached 1.6, a level last observed in September. The ratio is calculated as S&P 500 constituents with rising supply divided by those with falling supply. The higher the ratio, the more willing market makers are to sell the broad market. On 12/21 over 300 S&P 500 stocks had rising supply. Less than 200 had falling supply. Growing weakness over declining strength.

Finally, over 50% of the broad market was positioned in the weakness quadrant of our market structure map. The weakness quadrant is down-and-to-the-left, where current demand is below 30-day demand and current supply is above 30-day supply.

Since integrating market structure behavior into Point Focal in Q1-2021, I cannot recall seeing this quadrant so crowded. The average S&P constituent was 20% below its 30-day demand trend and 7% above its 30-day supply trend.

Low demand and high supply is a bearish divergence. Crowded weakness.

This view of market behavior is not driven by human biased headlines. It is constructed with rules-based explanations derived from market laws.

Specifically, short volume activity made possible by the SEC’s REG SHO short sale exemption for market makers. Plus 605 execution quality, 606 order routing regulations, and related reports.

The REG SHO exemption exists to facilitate orderly markets. It exempts market makers from having to borrow stock to short stock. The law removes friction from the process of market makers becoming short.

605 and 606 regulations exist to facilitate fair markets. They introduce transparency into venue decision making behavior - market participant interactions.

For a more thorough examination of market structure laws, spurious headlines, and why all market participants are not the same, see An Alt-Data Story Explainer.

With the market up about 1.5% on 12/21 CPI news stories, a client informed of the above, wrote, “Pretty big sell off coming based on that analysis?”

I responded, “I prefer Tim's language, which is to say that given this weak market structure profile, stocks are statistically less likely to achieve or sustain gains relative to stronger profiles. But yes, until these deteriorating trends halt and reverse, we should consider this a cautious-to-bearish input to trade strategies. In practice, thinking probabilistically, today's strength is a selling opportunity until the setup changes.”

12/22 saw the market give back the entirety of 12/21 gains. But one shouldn’t judge decisions on outcomes when thinking probabilistically1. Decisions should be made and judged based on the quality of information available at the time of the decision.

Understanding the relationship between market participant laws and behaviors enables us to derive and observe new market information. Short activity across a class of market participants. And a market participant interaction network.

Additive, high-quality information helpful to market entry and exit decision making.

Market structure demand and supply.

Strength and weakness.

From individuals to markets to the universe, stories are told and laws are observed. In all their chaos and beauty, through processes as measurable as the length of light in our days.

“The atoms of our body, as well, flow in and away from us. We, like waves and like all objects, are a flux of events; we are processes, for a brief time monotonous”

Carlo Rovelli, Reality Is Not What It Seems

Annie Duke, Thinking In Bets

.png)